Prof Eric Ghysels from the University of North Carolina at Chapel Hill presents an innovative approach to extracting factors which are shown to predict the VIX, the S&P 500 Realized Volatility, Variance Risk Premium and rare disaster fears.

The seminar is free and open to all. Seating is on a first-come, first-served basis.

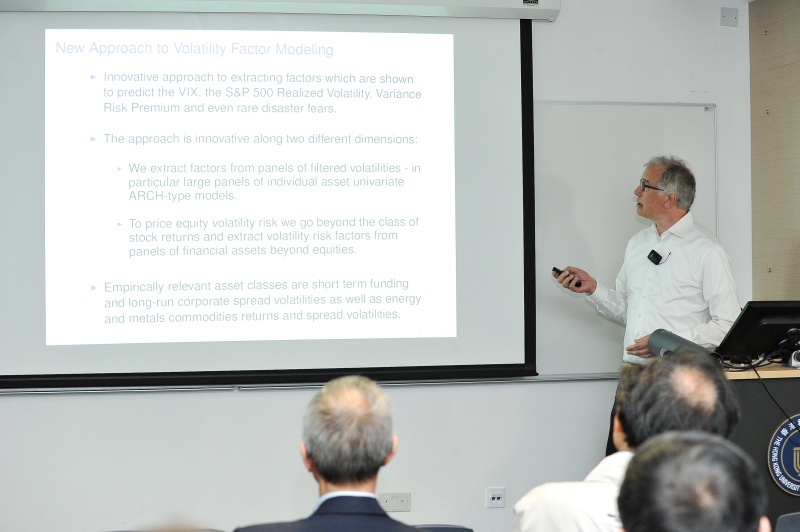

This talk presents an innovative approach to extracting factors which are shown to predict the VIX, the S&P 500 Realized Volatility, Variance Risk Premium and even rare disaster fears. The approach is innovative along two different dimensions, namely: (1) the speaker extracts factors from panels of filtered volatilities - in particular large panels of univariate financial asset ARCH-type models and (2) he prices equity volatility risk using factors which go beyond the equity class, and these are volatility factors extracted from panels of volatilities of short-term funding and long-run corporate spreads as well as volatilities of energy and metals commodities returns and sport/future spreads.

About the speaker

Prof Eric Ghysels received his PhD from Northwestern University in 1985. He was faculty at the University of Montreal from 1985 to 1996, and at Pennsylvania State University from 1996 to 2000. He joined the University of North Carolina at Chapel Hill in 2000, and is currently Bernstein Distinguished Professor of Economics and Professor of Finance.

Prof Ghysels’ main research interests are time series econometrics and finance. His most recent research focuses on Mixed Data Sampling (MIDAS) regression models and related econometric methods. Examples include MIDAS regression models involving data sampled at different frequencies which are of general interest. He was co-editor of the Journal of Business and Economic Statistics and is currently co-editor of the Journal of Financial Econometrics.

Prof Ghysels is a Fellow of the American Statistical Association and the Journal of Econometrics. He is also the Founding Co-President of the Society for Financial Econometrics.

The seminar is free and open to all. Seating is on a first-come, first-served basis.