Abstract

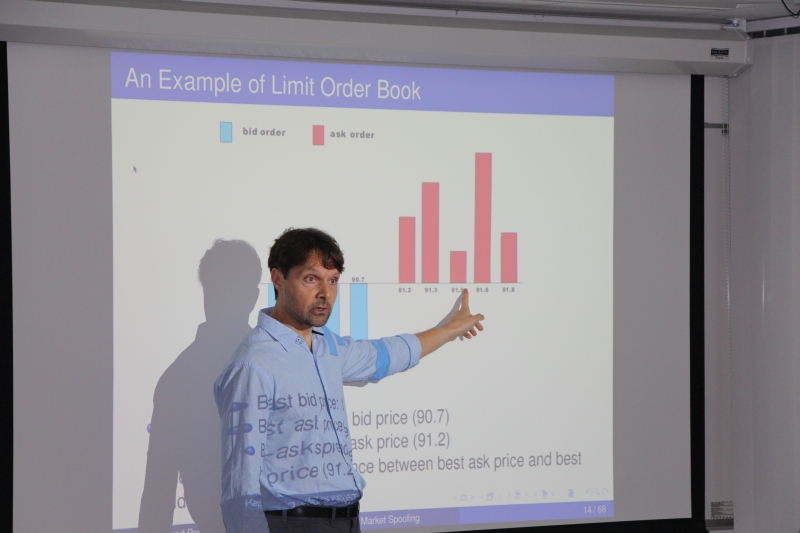

The speaker used a unique trading dataset of one week to analyze the behavior of high-frequency traders. About 8% of institutional traders intentionally or unintentionally first enter and then quickly cancel a buy (or sell) limit order without actually buying (or selling) before the trader actually sells (or buys) a security, and 45% of the institutions use this strategy at least once during the week. The total number of executions that is carried out by this strategy accounts for about 8% of all the executions of institutional traders for the purpose of proprietary trading. In this lecture, the speaker will show that the p-value for testing that all this behavior is a random event, and thus unintentional, is extremely small, equal to the probability of observing a 53-standard deviation event. Therefore, most likely at least part of the behavior is intentional and an indication of so-called “spoofing”, an attempt to manipulate prices. He will also show that on average, spoofing raises the return of a one-hour trade by 3 basis points and decreases the return of a three-hour trade against the spoofers by 6 basis points.

This is a joint work with Prof Xianhua Peng.

About the speaker

Prof Jussi Keppo received his D Tech in Applied Mathematics from Helsinki University of Technology in 1998. He then furthered his career in the Columbia University as a Postdoctoral Researcher and moved to University of Michigan as an Assistant Professor in 2000. In 2012, Prof Keppo joined the National University of Singapore and is currently the Associate Professor.

Prof Keppo’s research focuses on stochastic control; statistical analysis of stochastic processes and; optimization. His research was applied in risk management, information economics, investment under uncertainty, production optimization, and asset pricing.

Prof Keppo serves on the editorial boards of Mathematics of Operations Research, Journal of Risk, Production and Operations Management, and Journal of Energy Markets. He has consulted several Fortune 100 and asset management companies. He has several publications in the top-tier journals such as Journal of Economic Theory, Review of Economic Studies, Management Science, and Journal of Business on topics such as investment analysis, information economics, and banking regulation.

About the seminar series

For more information, please refer to the website http://ias.ust.hk/seminars/qfs/ for details.

|